Thailand, Indonesia, and Malaysia Are Building the Regulatory Infrastructure That Makes Fintech Entry Worth It

Three of Southeast Asia's most commercially significant fintech markets are simultaneously upgrading their regulatory infrastructure in 2026. Thailand is deepening cross-border payment linkages, Indonesia is opening digital banking to international players, and Malaysia's two-year digital insurer licensing window closes December 31. For financial brands watching from the outside, the window is narrowing.

For financial brands that have been watching Southeast Asia from a distance while waiting for regulatory clarity, 2026 is the year in which that clarity is actively being delivered across three of the region's most commercially significant markets. Thailand, Indonesia, and Malaysia are each at distinct but equally consequential stages of their fintech regulatory evolution. The regulatory frameworks being built or finalised in these markets this year will define the competitive architecture of their financial services industries for the next decade. The brands that engage with these frameworks now, while the application windows are open and the regulatory relationships are forming, will be operating from a structural advantage that will be difficult to replicate once those windows close.

Thailand: Cross-Border Payments and the PromptPay Infrastructure Advantage

Thailand has one of the most developed fintech regulatory environments in Southeast Asia, built on a payment infrastructure that the Chambers and Partners Fintech 2026 Thailand guide describes as firmly embedded in everyday commercial activity. PromptPay and the Thai QR Code payment rail account for approximately 44 percent of account-to-account electronic payments in the country, internet and mobile banking transaction volumes have continued to climb consistently through 2025, and the Bank of Thailand has maintained a regulatory posture that is simultaneously protective of consumer interests and supportive of fintech innovation.

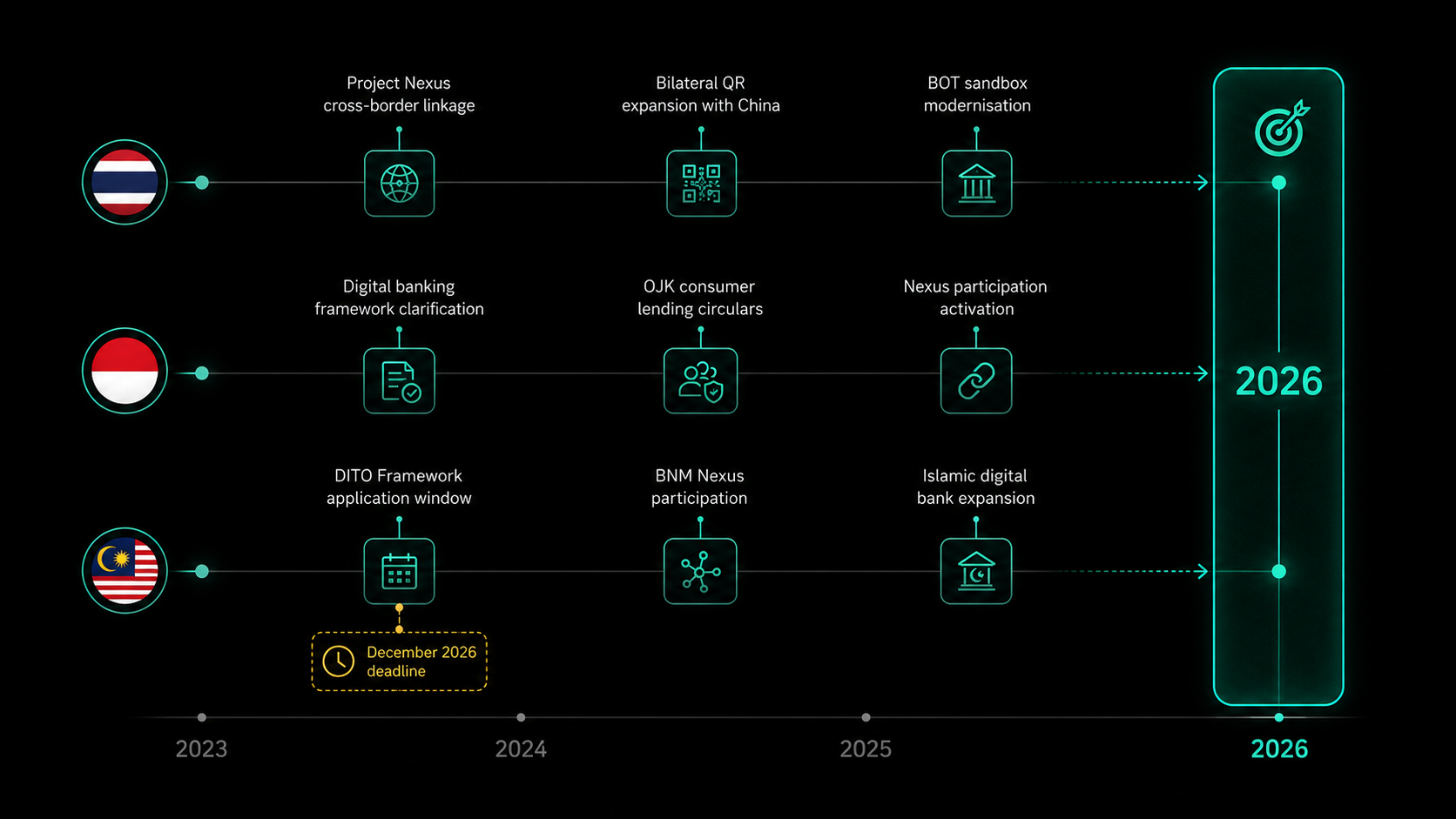

The most significant development in Thailand's fintech regulatory environment in 2026 is the deepening of cross-border payment linkages under Project Nexus, the Bank for International Settlements initiative connecting domestic instant payment systems across Malaysia, Indonesia, the Philippines, Singapore, and Thailand toward live cross-border implementation. In late 2025 and into 2026, Thailand also deepened bilateral QR linkages with China's Weixin Pay, Alipay, and UnionPay, creating direct payment connectivity with the world's largest digital payments market. For financial brands targeting Thai retail traders or serving Chinese tourists and investors in Thailand, these linkages change the practical accessibility of financial services in ways that directly affect client onboarding and deposit flow management.

Thailand's position as what the regulatory guides describe as a springboard into the wider Southeast Asian market is reinforced by the country's double taxation treaty network, which covers more than 60 jurisdictions as of 2026, and by the Bank of Thailand's regulatory sandbox framework that allows qualified financial technology firms to test products in a controlled environment before full market launch. For international financial brands that have been hesitating about Thailand entry due to regulatory uncertainty, the 2026 framework provides considerably more clarity and navigable pathways than were available three years ago.

Indonesia: The Largest Addressable Market Opening Further

Indonesia's fintech regulatory evolution in 2026 reflects the complexity of governing a 280 million person economy distributed across 17,000 islands, with a financial inclusion mandate that is both a commercial imperative and a social policy priority. The Financial Services Authority OJK has been systematically building the regulatory infrastructure that allows digital financial services to reach the underbanked majority of the Indonesian population while maintaining the oversight standards that protect consumers from the industrial-scale fraud operations that VIDA CEO Niki Luhur described at Money20/20 Asia as operating across the region.

The specific regulatory developments in Indonesia that are most relevant for international financial brands in 2026 involve the digital banking framework and the buy-now-pay-later and consumer lending regulations that have been clarified through OJK circulars issued in late 2025. Indonesia's digital banks, including Bank Jago in which GoTo has a significant stake, have demonstrated the commercial viability of mobile-first banking for the Indonesian consumer base in ways that have encouraged OJK to maintain an open and innovation-positive posture toward new entrants with credible financial backing and compliant operating structures.

The fintech funding landscape in Indonesia reinforces the regulatory openness. Singapore-based firms account for a disproportionate share of ASEAN fintech funding, but Indonesia remains the market where that funding is most actively deployed at the consumer level. DurianPay's 1,625 percent growth rate in the Financial Times APAC fastest-growing fintech list is a specific data point in a broader pattern of Indonesian B2B fintech infrastructure attracting both venture capital and strategic investment from regional players who recognize that Indonesia's scale, combined with the OJK's increasingly navigable regulatory framework, makes it the most significant growth market in Southeast Asia for any financial service provider with the patience to build locally.

Malaysia: The Digital Insurer Window and Islamic Finance Edge

Malaysia's regulatory environment for fintech in 2026 has two specific time-sensitive elements that financial brands need to be aware of. The first is Bank Negara Malaysia's Digital Insurer and Takaful Operator framework, published in July 2024, which opened a two-year application window from January 2025 through December 31, 2026 for new digital insurance and takaful operators to apply for licenses. This window closes at the end of 2026. Financial brands with insurance or protection product ambitions in the Malaysian market that have not yet assessed this framework are running out of time to do so before the application period closes.

The second is Malaysia's participation in Project Nexus, which will create a direct instant payment linkage between the Malaysian DuitNow system and the equivalent systems of Singapore, Thailand, Indonesia, and the Philippines. The commercial implication for financial brands serving regional clients or facilitating cross-border financial activity is that Malaysia's payment infrastructure will become significantly more interoperable with the broader ASEAN payment ecosystem over the next 12 to 24 months, reducing the friction for cross-border financial services that currently requires workarounds through international banking relationships.

Malaysia's Islamic finance infrastructure is the dimension of its financial regulatory environment that receives the least attention from international financial brands and represents the most significant strategic gap. Malaysia is one of the world's leading Islamic finance jurisdictions, with Sharia-compliant financial products embedded throughout its banking, insurance, and capital market infrastructure in ways that have no equivalent in any other ASEAN market. Aeon Bank, the first Islamic digital bank to launch in Malaysia, did so in May 2024 and has since partnered with Zurich Malaysia for inclusive takaful products and with Visa for Sharia-compliant digital payments. For financial brands whose target client base includes Malaysia's Muslim-majority consumer population, Islamic finance compliance is not a regulatory checkbox. It is a product and brand strategy requirement.

In Malaysia, Islamic finance compliance is not a regulatory checkbox for international financial brands. It is a product strategy requirement that determines whether the majority of the market considers you at all.

What Operators Should Be Doing Before the Windows Close

The regulatory developments across Thailand, Indonesia, and Malaysia in 2026 share a common characteristic that makes them strategically significant beyond their individual jurisdictional relevance: they are happening simultaneously, they are creating new points of entry and new competitive requirements at the same time, and they are establishing the frameworks that will define market structure for the next decade. The brands that engage with these frameworks now, that build the regulatory relationships and compliance infrastructure that the 2026 environment rewards, are making investments that compound as the frameworks mature and as the competitors who waited for certainty discover that the windows have closed.

The practical first step for international financial brands is not regulatory analysis in isolation. It is market intelligence that connects the regulatory developments to the specific commercial opportunities and constraints that are relevant to their product profile, their target client segment, and their existing regulatory standing. Thailand's cross-border payment linkages matter differently for a broker that is primarily serving Thai retail traders than for one that is focused on serving Chinese investors with Thai-market access. Indonesia's OJK framework matters differently for a digital lending platform than for a traditional CFD broker. Malaysia's Islamic finance infrastructure matters differently for a brand targeting the Malay-majority retail market than for one primarily serving the Chinese-Malaysian trading community. The regulatory environment is the structural context. The commercial strategy is the translation of that context into specific and actionable market entry or expansion decisions.