Robinhood Just Let AI Agents Take the Wheel on Retail Portfolios

On May 26, 2026, Robinhood launched Agentic Trading, allowing third-party AI assistants to buy and sell stocks on behalf of its 27.5 million customers with minimal human involvement. The Nasdaq closed at a record 26,972 today. Nobody has seriously asked what happens when the agents are wrong at scale.

On Wednesday May 26, 2026, Robinhood announced two new products: Agentic Trading and an Agentic Credit Card. The products allow customers to connect third-party AI assistants to their Robinhood accounts, authorise those assistants to execute trades and make purchases on their behalf, and then step back. The AI does the rest. On Friday May 30, the Nasdaq Composite closed at 26,972.62, up 0.2 percent on the day and up 8 percent for the month of May, a record. The S&P 500 closed at 7,580.06, also a record. Dell Technologies surged 33 percent, its best single day on record, after reporting AI server orders exceeding $12 billion year-to-date. Mizuho surveyed Robinhood users and found that approximately 89 percent said they would likely consider opening a dedicated Agentic Trading account.

Those two things, the launch of autonomous AI trading for retail investors and the stock market closing at all-time highs on AI-driven earnings, happened in the same week. They are related. They are also, in combination, the most consequential and least interrogated development in retail financial markets since the zero-commission trading revolution that Robinhood itself launched in 2013. The questions that have not yet been asked about agentic trading at scale are the ones that will define the next chapter of retail financial market structure, in the United States and, given the speed at which financial technology innovations travel from Silicon Valley to Southeast Asia, across every retail trading market in the world.

What Agentic Trading Actually Is and Is Not

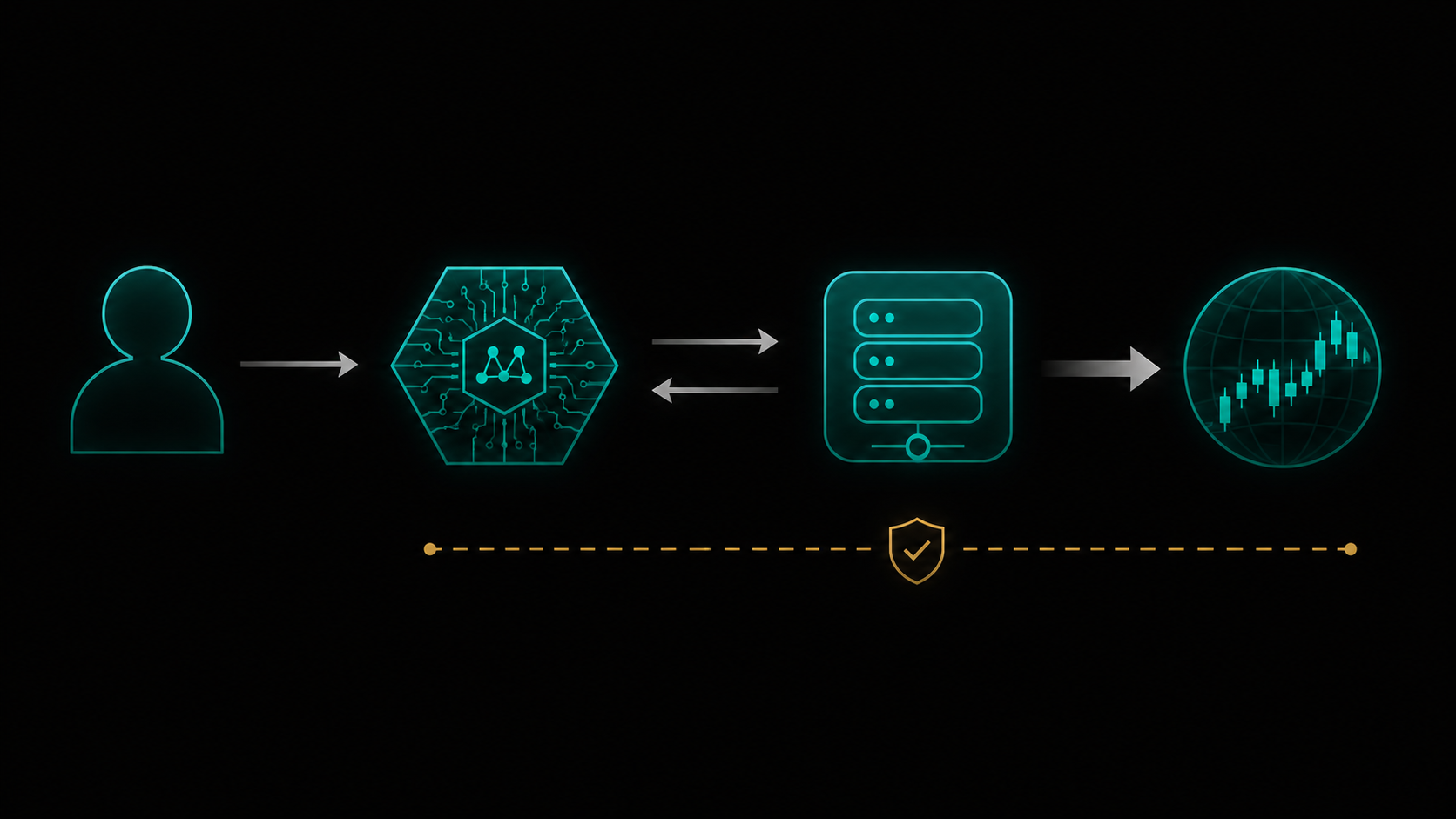

According to CNBC's May 27 report, Robinhood's Agentic Trading allows customers to connect third-party AI assistants to a dedicated account, separate from their main portfolio, and instruct those agents to rebalance portfolios, monitor themes such as AI stocks, or execute trading strategies automatically. The agent reads and analyses the user's portfolio, generates trading strategies, and places orders against a pre-loaded balance in the dedicated wallet. A real-time activity feed shows what the agent has done. Users can disconnect the agent instantly with a single tap.

The "third-party AI assistants" language is important. Robinhood is not itself the AI. It is the marketplace and the execution rail. Customers connect whatever AI agent they choose, whether that is a product from OpenAI, Anthropic, Google, or a smaller specialized financial AI provider, to their Robinhood account via what the company describes as its Model Context Protocol integration. The AI agent operates within spending limits the user sets and with fraud monitoring from Robinhood's own team. Current agentic trading is limited to equity trading, with options, crypto, event contracts, and futures trading expected to follow after testing.

The TechCrunch coverage noted that this makes Robinhood one of the first platforms to bring autonomous finance technology to ordinary investors rather than institutions. That framing is accurate and it is the commercial and regulatory frontier that the launch defines. Algorithmic and AI-assisted trading has existed in institutional finance for decades. What is new is not the technology. What is new is the democratization of that technology to retail investors who, by definition, do not have the risk management infrastructure, compliance frameworks, or market sophistication that institutional actors deploy around algorithmic trading systems.

The 89 Percent Adoption Signal and What It Means

Mizuho's survey of Robinhood users, cited in CNBC's May 30 market wrap, found that approximately 89 percent of respondents said they were likely to consider opening a dedicated Agentic Trading account. The average portfolio allocation they were willing to commit to agentic management was 31 percent. And 26 percent of non-Robinhood respondents said the agentic trading feature made them open to considering opening an account.

These are not speculative projections. They are survey data from the existing customer base of a platform with 27.5 million users and first-quarter 2026 equity trading volumes of $638 billion, up 54 percent year over year. Robinhood's CEO Vlad Tenev said at launch: our mission has always been to democratize finance for all, and now, that mission extends to AI agents. The Mizuho analyst covering the stock raised the price target to $115 from $110, describing agentic trading as a strong customer acquisition tool.

The 89 percent adoption intent figure is commercially extraordinary. It is also, depending on how you read it, either the clearest possible signal of retail investor enthusiasm for AI-assisted finance, or the clearest possible signal of how little the retail investor audience has interrogated what they are agreeing to. These two readings are not mutually exclusive. Both can be true simultaneously, and the history of retail financial innovation suggests that high adoption intent at launch frequently precedes the discovery of structural risks that were not visible to early adopters in a bull market.

The Questions Nobody Is Asking During a Record Rally

The week of Robinhood's agentic trading launch was also the week the Nasdaq gained 8 percent in May and hit a closing record of 26,972. Dell surged 33 percent on AI server earnings. The PHLX Semiconductor Index outperformed. The S&P 500 first-quarter earnings beat rate reached 83 percent of reporting companies, against a long-term average of 67 percent. In this environment, the questions about agentic trading are not being asked with any urgency, because the agents, if anyone had been running them, would have been profitable simply by holding positions in the direction of the market.

The questions become urgent the moment the market direction reverses. Consider the specific structural risks that have not yet been publicly addressed by Robinhood, by its regulators, or by the financial press covering the launch.

- Correlated AI behaviour: If a significant proportion of Robinhood's 27.5 million users connect the same or similar AI agents, those agents will respond to the same market signals with the same trading logic at the same time. The result is correlated selling or buying at scale from a retail investor base that was previously fragmented in its decision-making. The market impact of correlated AI behaviour across millions of retail accounts has not been modelled publicly.

- Liability and accountability: When an AI agent executes a trade that results in a significant loss, who is liable? The user who authorised the agent? The AI provider whose model generated the trading strategy? Robinhood, which provided the execution infrastructure? The legal framework for allocating liability across this three-party arrangement does not yet exist in any jurisdiction.

- Regulatory jurisdiction: The SEC's existing rules on investment advice, fiduciary duty, and suitability were written for human advisors and algorithmic trading systems operated by registered firms. A third-party AI agent operating on a retail investor's account sits in a regulatory gap that neither the SEC nor FINRA has publicly addressed as of the launch date.

- Adversarial manipulation: AI agents that are trained on market data and news can be influenced by the quality of that data. A coordinated campaign of false or misleading market signals, targeting the training data or real-time inputs of widely-used AI trading agents, represents a market manipulation vector that did not exist before agentic trading became available to retail investors.

- Cascade risk in volatile conditions: The April 2026 oil market demonstrated that a single Trump social media post can move Brent crude 10 percent in a session. AI agents trained to respond to news sentiment and market signals would respond to such events at machine speed, potentially amplifying the initial move before any human circuit breaker could activate.

None of these risks are hypothetical. Each has direct precedents in the history of algorithmic trading at the institutional level, where they have produced the 2010 Flash Crash, the 2012 Knight Capital incident that lost $440 million in 45 minutes due to a software error, and numerous smaller but structurally equivalent episodes of automated trading amplifying market dislocations. The difference between those precedents and the current situation is that they involved regulated, professionally managed trading systems with risk controls designed by experienced engineers with compliance oversight. Agentic trading at Robinhood is a consumer product available to investors who may have never bought a stock before, as Vlad Tenev's own framing explicitly acknowledged.

89 percent of users want to hand their portfolios to an AI. Nobody has publicly modelled what happens when those agents all receive the same signal and act at the same moment.

The Regulatory Silence That Is Itself a Signal

The SEC has not issued guidance on agentic trading. FINRA has not issued guidance on agentic trading. The Consumer Financial Protection Bureau has not issued guidance on agentic trading. The Fortune coverage of the Robinhood launch noted the new questions the product raises about autonomy and risk but did not cite any regulatory response. The TheStreet report covered the product in broadly positive terms, noting the fraud detection protection and the instant disconnect feature as safeguards.

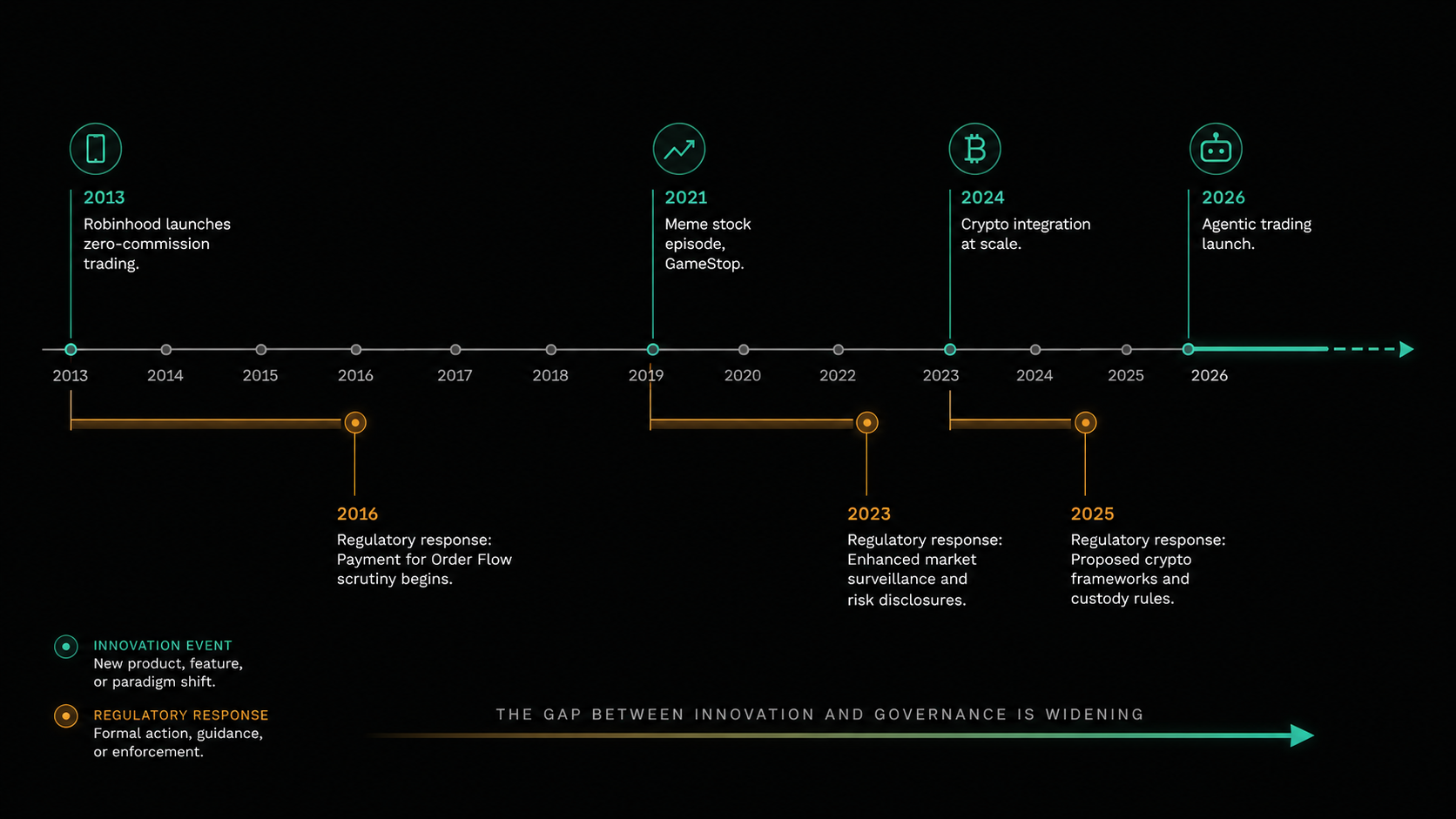

The regulatory silence is not surprising. It follows the established pattern of retail financial innovation in the United States, where new products are launched, adopted at scale, and then regulated retroactively after a problem of sufficient size has materialized. Zero-commission trading was adopted by tens of millions of users before the payment for order flow controversy produced its first congressional hearing. The meme stock episode of early 2021 occurred before any regulatory framework for coordinated retail trading behaviour existed. Crypto was integrated into retail platforms before any comprehensive federal framework for digital assets was passed.

In each of these cases, the retroactive regulation was triggered by a loss event significant enough to produce political pressure for a legislative response. The question for agentic trading is not whether that loss event will occur. It is when, what form it will take, how large it will be, and which regulatory authority will claim jurisdiction over a product that sits simultaneously in the categories of investment advice, algorithmic trading, consumer financial services, and artificial intelligence.

Why This Matters for Financial Brands in Asia Pacific

Robinhood's agentic trading product is currently a US-only launch. But the direction of travel it represents is not US-specific. Vanguard's own analysis described agentic AI as the big unlock for investors. Google, OpenAI, and Circle have all joined to develop standards for agentic payments. Kevin Bessent and Jerome Powell discussed AI risks in what was described as a high-stakes meeting. The institutional consensus is not that agentic trading is a niche product. It is that agentic trading is the direction in which all retail financial platforms are heading.

For regulated financial brands operating across Southeast Asia, this development has two immediate strategic implications. The first is competitive: the retail trading and investment audience across Thailand, Vietnam, Indonesia, Malaysia, and the Philippines is the same audience that is watching Robinhood's product launches and forming expectations about what financial technology should be capable of delivering. The brands that will define the agentic trading narrative in these markets before the first major agentic trading product reaches them, by producing clear, honest, locally relevant analysis of what these tools can and cannot do, what the risks are, and what questions regulators have not yet answered, are positioning themselves as the trusted analytical voice on a topic that will dominate retail financial media in the second half of 2026.

The second implication is structural. Southeast Asian financial regulators, including the MAS in Singapore, the SEC in Thailand, OJK in Indonesia, and the Securities Commission in Malaysia, will all be watching the Robinhood experiment. The regulatory frameworks they develop for agentic trading in their own jurisdictions will be shaped in part by how the US experience unfolds. The financial brands that build their authority as credible, analytically sophisticated voices on the intersection of AI, autonomous trading, and retail investor protection in 2026 will be the brands whose input regulators seek when the frameworks are being written. That is a commercial and reputational positioning opportunity that is available right now, and that will narrow considerably once the topic becomes widely contested.