Financial Brands Lose the Trust War in Southeast Asia

Regulated credentials, competitive spreads, and media spend are not enough. Foreign financial brands entering Southeast Asia fail on a structural gap that advertising cannot close: the absence of local authority.

The pattern repeats across markets and across cycles. A foreign financial brand, regulated, capitalised, and genuinely competitive on product, enters Thailand, Vietnam, or Indonesia with a marketing plan built on performance advertising, a translated website, and a brand deck that leads with its FCA or ASIC license. Six months later, the cost per acquisition is higher than projected, conversion rates are below target, and churn is running at levels that make the unit economics difficult to defend. The product has not failed. The trust architecture was never built.

The Structural Gap That Advertising Cannot Close

The Edelman Trust Barometer 2026 surveyed 34,000 respondents across 28 countries and found that seven in ten people globally report distrust toward brands from unfamiliar backgrounds. For financial brands specifically, the trust gap between foreign entrants and locally familiar names runs to 15 points on average. In Indonesia, that deficit widens to 26 points. These are not soft perception metrics. They translate directly into conversion rates, cost per acquisition, and the lifetime value of clients who leave when a competitor offers a marginally better bonus structure.

The temptation is to treat this as a media problem solvable with more spend. It is not. The retail forex and CFD trading audience across Southeast Asia is among the most community-oriented financial audience in the world. Before opening an account, a trader in Vietnam or Malaysia will search the broker name in their native language, cross-reference it on platforms like TrustFinance and ask peers in their Telegram or Facebook trading communities. What they find in those searches, and what they do not find, shapes the decision more than any paid placement. A brand with no local-language media presence, no community visibility, and no independent verification signals is invisible to that process regardless of how much it has spent on Google keywords.

This is the structural gap. Not product quality, not pricing, not even regulatory standing. The gap is the absence of the independent, locally grounded trust signals that Southeast Asian retail traders use as their primary evaluation mechanism, and that no advertising budget can substitute for.

Local Media Is Verification Infrastructure, Not PR

The function of local media coverage for a financial brand entering Southeast Asia is not awareness in the conventional marketing sense. It is verification. When a potential client searches a broker name in Thai or Vietnamese and finds editorial coverage from recognised local financial outlets, that coverage is not just information. It is independent third-party validation from sources the audience already trusts. The inference the audience makes, that a journalist or publication with a reputation to protect considered this brand worth covering, lowers the perceived risk of engaging with a foreign financial brand significantly.

The secondary function of local media coverage is search presence in the language the audience actually uses. A broker that has generated local-language press appears in local-language searches. A broker that has not is dependent entirely on paid search to be visible at the moment a potential client is conducting their research. The cost differential between organic earned media presence and perpetual paid search dependency, compounded across a 12-month market entry period, is large enough to materially affect the economics of regional expansion.

Thailand has a developed retail trading media ecosystem spanning dedicated forex news platforms, financial press with active trading sections, and a community media layer consisting of YouTube channels and Telegram communities with substantial engaged audiences. Vietnam is in active transformation, accelerated by its FTSE Emerging Market reclassification taking effect in September 2026. Malaysia and Indonesia represent the two largest retail trading audiences in ASEAN where international financial brands have systematically underinvested in local-language media presence, focusing instead on English-language regional outlets that reach a professional and institutional audience but miss the retail trading population that represents the growth opportunity.

Community Credibility Cannot Be Purchased

In Southeast Asian trading markets, the review and community layer operates with a directness that has no equivalent in Western financial markets. TrustFinance , ForexPeaceArmy, and their regional equivalents are actively and routinely consulted by retail traders before making any account opening decision. A brand with strong review signals on these platforms has a compounding trust advantage. A brand with gaps or negatives carries a burden that no campaign can fully offset without first addressing the underlying perception problem directly.

- Review platforms including TrustFinance and ForexPeaceArmy are consulted by traders across Thailand, Vietnam, Indonesia, and Malaysia before account decisions, making profile management a commercial priority rather than a reputation afterthought.

- Telegram trading communities in Southeast Asia range from a few hundred to tens of thousands of members, and the most respected channels generate word-of-mouth that no paid placement can replicate at equivalent quality.

- Copy trading ecosystems and signal provider networks create secondary trust transfer mechanisms, where a respected community trader's broker preference carries disproportionate influence with their audience.

- YouTube trading educators in local languages represent some of the highest-trust information channels for retail traders in the region, and their broker associations are evaluated as implicit endorsements by their audiences.

The brands that have built durable positions in these community layers did not do so through community manager hires or sponsored posts. They did so by being genuinely present, over time, with content that demonstrated actual market knowledge and treated the community as peers rather than targets. That distinction is perceptible to a Southeast Asian trading community that has had years of exposure to brands that treat them as acquisition funnels.

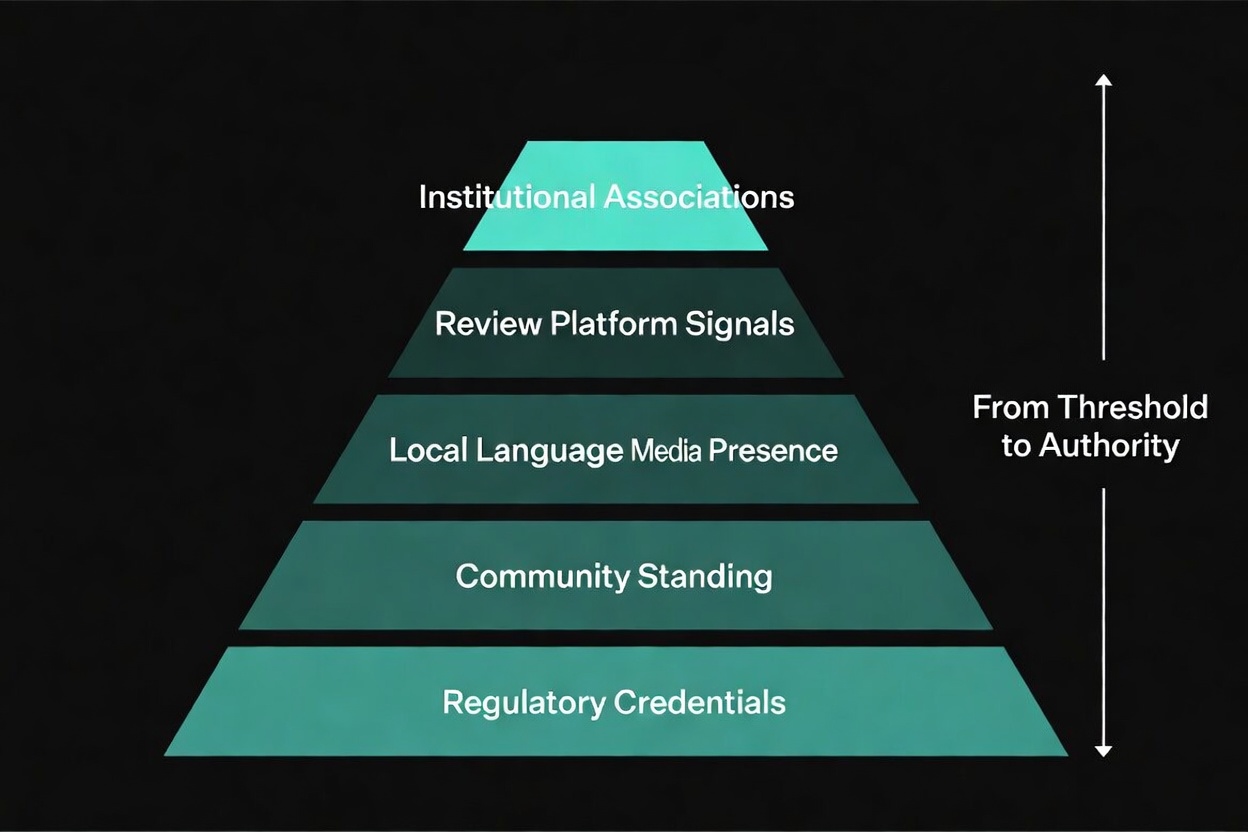

Institutional Association Provides the Credibility Floor

Institutional associations, most effectively through university-level trading education programs, create a trust signal that community presence and media coverage cannot fully replicate. When a financial brand delivers a certified trading education workshop in partnership with a Vietnamese or Malaysian university, it has done something categorically different from advertising. It has created a physical room of people who encountered the brand in a context that their own reference systems, family expectations, and peer networks identify as legitimate. The university's credibility extends to the brand by association, and that association travels through the communities those students belong to well beyond the event itself.

The regulatory goodwill dimension compounds the community benefit. Regulators in Vietnam and Malaysia have both expressed consistent concern about financial literacy gaps in their retail investment markets. A financial brand that is actively and visibly addressing those gaps through formal institutional partnerships occupies a different regulatory posture than one that is purely extracting from the market. That posture is not a compliance strategy. It is a brand strategy with commercial consequences that show up in conversion rates, regulatory scrutiny levels, and the quality of the institutional relationships that define long-term market access.

Zero press in a target market is not a neutral condition. It is a disqualifier, read by the retail audience as evidence that the brand does not know the market well enough to care.

The Sequence That Separates Winners from Late Arrivals

The brands that currently lead on market share in Southeast Asian retail trading markets share a recognisable pattern in how they built their positions. They invested in authority before they invested in acquisition. They treated local-language media presence as infrastructure rather than output. They built community standing through sustained participation rather than campaign activation. And they established institutional associations before they needed them as credibility insurance.

The timing dimension is commercially consequential. Vietnam's FTSE reclassification in September 2026 will bring a wave of institutional capital and global brand attention to a market that is, as of today, still building its retail financial media ecosystem. The brands building Vietnamese-language content, community relationships, and institutional associations in the six months before September are investing at a moment when the competitive cost of establishing that presence is lower than it will be in the 12 months that follow. Thailand rewards the same logic: the brands with the deepest local media presence and community standing consistently outperform new entrants on conversion regardless of product parity, because the trust layer was built before the acquisition pressure arrived.

Indonesia remains the clearest example of the gap between market opportunity and brand investment quality. With more than 280 million people and GDP growth consistently above 5 percent, it represents the largest single addressable retail financial audience in Southeast Asia. Most international financial brands are entering it with strategies designed for smaller, more compact markets: translated advertising, generic social media presence, and English-language brand positioning that the Indonesian retail trading audience correctly reads as evidence that the brand does not understand them. The brands that invest in genuine Bahasa Indonesia editorial content, authentic engagement with Indonesian trading communities, and the patience to build review platform credibility before acquisition pressure mounts will find the market materially more accessible and the client relationships materially more durable.

What This Means for Operators

The argument here is not that performance advertising is wasteful or that community investment is sufficient on its own. The argument is sequential. In markets defined by the trust dynamics of Southeast Asia, performance advertising converts most efficiently when the independent trust signals are already in place to answer the verification searches that follow every paid click. The brands that have built those signals in advance are buying media in a market where their brand can be verified. The brands that have not are buying media in a market where their brand disappears the moment a potential client conducts a native-language search, checks a review platform, or asks a community they trust. The investment case for building the trust layer before scaling the acquisition layer is not strategic theory. It is the operational logic of the brands that are winning this market right now, expressed in their cost per acquisition numbers and their client retention rates.