APAC Fintech Is Growing at Full Speed Into an Industrial-Scale Fraud Crisis

Southeast Asia now dominates global fintech expansion plans, with digital payments projected to exceed $1.5 trillion in 2026. At the same moment, fraud across the region has reached what regulators and industry leaders are calling industrial scale, with synthetic identity attacks up 142 percent and deepfake fraud surging over 1,500 percent in Singapore alone. The two stories cannot be separated.

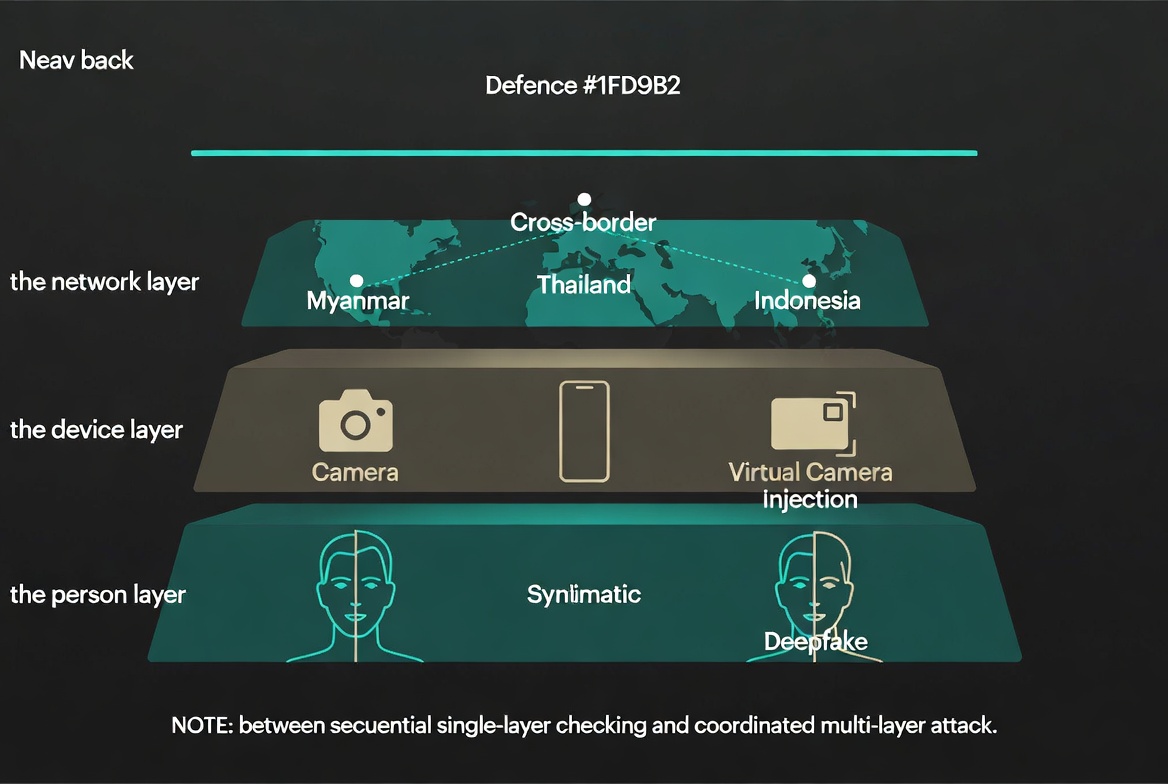

At Money20/20 Asia 2026 in Bangkok, Niki Luhur, founder and CEO of Indonesian digital identity network VIDA, delivered a warning that was unambiguous in its framing. Fraud across Southeast Asia, he told the audience, has reached an industrial scale. Cross-border syndicates operating between Myanmar, Thailand, and Indonesia have transformed what was once isolated criminal opportunism into a high-volume, systematised enterprise. He cited a $12 billion Bitcoin seizure in Myanmar as a single data point illustrating the magnitude. The conference room was full of fintech executives who had gathered to discuss the future of embedded finance, AI-driven banking, and cross-border payment innovation. The context of that conversation, a region simultaneously breaking records on digital financial adoption and confronting fraud infrastructure that rivals the scale of the legitimate industry it is targeting, defines the strategic situation for every financial brand operating across Asia Pacific in 2026.

The Money20/20 Future of Fintech in APAC 2026 report, based on surveys and interviews with more than 130 senior fintech leaders across Asia, confirms the headline numbers that frame this tension. Southeast Asia dominates fintech expansion plans, with 22.9 percent of APAC respondents identifying the region as their primary growth target. Digital payment transactions across the region are projected to exceed $1.5 trillion in 2026. Financial inclusion is now a commercial imperative rather than a corporate social responsibility exercise, with 90.6 percent of executives stating that social good initiatives are embedded in corporate strategy. And 63.5 percent of fintech leaders identify fraud prevention as their top operational priority for the year, a figure that would have been inconceivable in the 2021 or 2022 editions of the same survey.

The Fraud Numbers That Are Not in the Pitch Decks

The Sumsub APAC Fraud 2026 report documents a 142 percent rise in synthetic identity fraud across the Asia Pacific region. Synthetic identity fraud, in which fraudsters combine real identity data such as a valid national ID number with fabricated personal details to create a composite persona that passes automated verification checks, has become the dominant fraud vector in APAC's financial sector because it exploits the specific weakness of the KYC frameworks that most digital financial platforms deployed during the rapid onboarding cycles of 2021 to 2024. Those frameworks were designed to reduce friction for legitimate users. They were not designed to detect identities that are 60 percent real.

The deepfake dimension is structurally more alarming because it is accelerating faster than any defensive measure is being deployed. Singapore recorded a 1,500 percent surge in deepfake fraud cases in a single year, according to Sumsub's research. Hong Kong SAR recorded a 1,900 percent jump over the same period. Malaysia recorded deepfake-related fraud growth exceeding 400 percent year on year. These are not marginal statistical movements. They represent a wholesale shift in the fraud capability available to organised criminal networks in the region, enabled by generative AI tools that have become accessible at consumer price points.

Luhur's specific technical warning at Money20/20 Asia is worth quoting directly in its framing. He noted that while deepfakes dominate media coverage of AI-enabled fraud, the actual operational threat that is most difficult to detect is injection attacks: fraudsters using virtual cameras on compromised devices to inject pre-recorded or AI-generated video into liveness verification sessions, making a synthetic face appear to pass real-time biometric checks. The distinction matters because injection attacks defeat the specific security layer that most financial platforms have deployed as their primary defence against deepfake fraud. A platform that has invested in facial liveness detection as its anti-fraud measure is potentially no more secure against a sophisticated injection attack than one that has not, if the injection occurs before the liveness check rather than during it.

Vietnam's Biometric Mandate and What It Signals for the Region

Vietnam's regulatory response to the fraud crisis is the most structurally significant government action in the region in 2026, because it establishes a precedent that neighbouring regulators are watching closely. From January 2026, Vietnam made biometric identity verification mandatory for opening any new bank account or payment card. Banks are required to verify a customer's face either in person or via a trusted biometric database before activating any financial service. The State Bank of Vietnam's framework is explicit: digital banking growth must be anchored to higher-assurance identity verification, not optimised onboarding funnels.

The commercial consequences of this mandate are significant for any fintech or financial brand that has built its Vietnam market entry strategy around the low-friction digital onboarding experience that was the competitive standard in 2023 and 2024. Vietnam's regulatory shift does not reduce the size of the market opportunity. The FTSE Emerging Market reclassification taking effect in September 2026 will bring substantial institutional capital flows into Vietnamese financial markets, expanding the retail investor and trading audience significantly. But it changes the compliance baseline that financial brands must meet to operate in the market, and it signals the direction that other ASEAN regulators are likely to follow.

Cake Digital Bank's response to the Vietnam mandate is instructive. The digital-only bank became the first in Southeast Asia to pass iBeta Level 2 testing for face biometric spoofing detection, deploying passive liveness detection across its millions of users to meet the State Bank's requirements. The competitive implication is direct: in a market where biometric verification is mandatory and the testing standards for that verification are documented and publicly benchmarked, the brands that invest in the highest-assurance verification infrastructure are not just complying with regulation. They are creating a trust differentiation that the retail consumer can evaluate, the most commercially valuable form of regulatory compliance available.

The Trust Verification Ecosystem That Retail Traders Actually Use

The fraud crisis in APAC fintech is not only a KYC and onboarding problem. It is a trust evaluation problem that operates through the research behaviour of retail financial consumers across the region. Before opening a trading or investment account with any financial brand, a retail trader in Thailand, Vietnam, Indonesia, or Malaysia will conduct a verification process that has become increasingly structured as the number of scam platforms has increased and the sophistication of fraudulent brand impersonation has grown.

That verification process runs through multiple channels simultaneously. It includes regulatory status checks on the relevant national regulator's public registry. It includes community consultation through Telegram groups, Facebook trading communities, and peer networks where broker reputations are discussed in real time. It includes platform-specific review and rating searches, where services like TrustFinance, WikiFX, and ForexPeaceArmy provide aggregated trader reviews, regulatory status information, and fraud alert systems that the retail audience has learned to consult before committing any capital. And it includes local-language media searches, where the presence or absence of independent editorial coverage functions as a credibility signal that paid advertising cannot replicate.

The role of review and verification platforms in this ecosystem is commercially significant in ways that most international financial brands entering Southeast Asian markets have underestimated. TrustFinance specifically addresses the retail trader's core verification need: an independent, structured assessment of whether a financial brand can be trusted, based on regulatory compliance, client reviews, and fraud signal monitoring. In a market environment where synthetic identity fraud has risen 142 percent and deepfake-enabled scam platforms have reached industrial sophistication, the retail trader's need for independent third-party verification of a broker's legitimacy is not a peripheral concern. It is the primary decision gate between brand awareness and account opening.

- Regulatory registry checks: retail traders in Thailand, Vietnam, Malaysia, and Indonesia routinely cross-reference broker names against the SEC Thailand, OJK, SC Malaysia, and SSC Vietnam public registries before any account decision, making unregistered or clone broker operations immediately identifiable to informed traders.

- Community peer verification: Telegram trading groups ranging from hundreds to tens of thousands of members function as real-time fraud alert networks, where a newly identified scam platform or broker withdrawal complaint travels through the community faster than any formal regulatory warning.

- Third-party review platforms: services including TrustFinance, WikiFX, and ForexPeaceArmy aggregate trader reviews, regulatory status data, and fraud alerts into structured trust assessments that retail audiences consult as standard pre-account research.

- Local-language editorial search: the presence of independent Thai, Vietnamese, Bahasa Indonesia, or Bahasa Malaysia coverage of a financial brand in recognised local media functions as an implicit verification signal that the brand is legitimate enough to be reported on by journalists with reputations to protect.

- Social proof and copy trading networks: signal providers and copy trading educators with established community followings generate secondary trust transfer when they publicly associate with specific brokers, carrying the credibility of the educator to the brand through the trading community's trust in that educator.

Trust is the new currency of digital finance, and the companies that embed it in every interaction while delivering a frictionless experience will define the future of the industry.

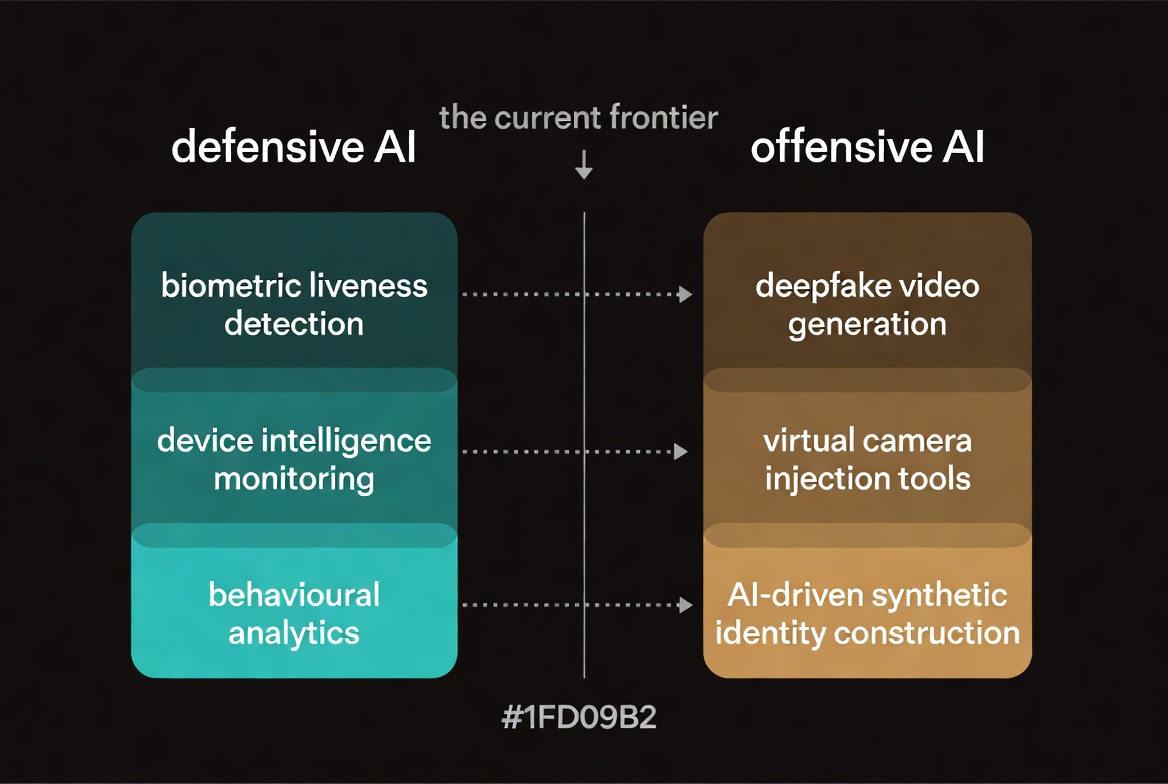

AI Adoption Is Accelerating on Both Sides of the Fraud Line

The Money20/20 Future of Fintech APAC 2026 report found that 61.2 percent of APAC fintech organisations are accelerating AI adoption in 2026, with the primary use cases spanning fraud detection, credit scoring, personalised financial services, and regulatory compliance automation. The same report found that 70 percent of APAC organisations expect agentic AI to disrupt their business models by end of 2026, a finding that sits in direct dialogue with Robinhood's May 26 launch of autonomous AI trading for retail investors in the United States.

The challenge for APAC fintech operators is that AI is being adopted simultaneously by the fraud infrastructure they are defending against. Sumsub's research identifies AI-driven fraud agents as an emerging threat category: autonomous systems that use generative AI, automation, and behavioural mimicry to carry out full verification attempts from start to finish, without any human involvement in the attack. These systems can generate synthetic identity documents, produce deepfake video for liveness checks, mimic human typing and interaction patterns to defeat behavioural biometrics, and route attacks through compromised legitimate devices to defeat device intelligence systems, all in a coordinated sequence that a single-layer defence cannot detect.

VIDA's proposed solution, which it launched at Money20/20 Asia as ID FraudShield, addresses this by combining biometric liveness detection, device intelligence, behavioural analytics, and network detection into a simultaneous multi-layer verification architecture. The commercial logic is that no single defence layer is sufficient against a multi-layer attack, and that the verification architecture of legitimate financial platforms needs to match the coordination architecture of the fraud networks it is defending against. This principle, simultaneous verification of person, identity, and device rather than sequential checking of each, is what Vietnam's biometric mandate is beginning to codify in regulatory requirements, and what the broader ASEAN regulatory community is watching to determine whether to adopt.

What This Means for Financial Brands Entering the Region

For regulated financial brands and forex brokers building market entry strategies for Southeast Asia in 2026, the convergence of unprecedented growth and industrial-scale fraud creates a specific and commercially consequential strategic requirement. The brands that treat the trust and verification infrastructure of the region as a compliance cost to be minimised are misreading the competitive landscape. In a market where retail traders have learned to verify broker legitimacy through multiple channels before opening any account, where platforms like TrustFinance provide structured independent assessments that the retail audience actively consults, and where fraud awareness has been elevated by years of high-profile scam platform exposure, the verified trust signal is not a threshold that brands clear on their way to marketing. It is the marketing.

The brands winning client acquisition in Southeast Asian retail financial markets in 2026 are those that have built their presence across every layer of the trust verification ecosystem that their target audience uses. They have active, accurate, and positively maintained profiles on the review and verification platforms that retail traders consult. They have local-language editorial coverage from recognised media that functions as independent credibility confirmation. They have community standing in the Telegram and social trading networks where broker reputations are discussed. And they have the regulatory compliance infrastructure, including, increasingly, biometric verification standards aligned with the direction regulators are taking across the region, that protects them from the scam broker association that high fraud rates have made a constant reputational risk for any foreign financial brand in these markets.

The Money20/20 APAC report's framing that Southeast Asia is no longer just an emerging market but the global testing ground for the future of finance is commercially accurate. What it does not capture is the corollary: a market that is the global testing ground for the future of finance is also the global testing ground for the future of financial fraud. The brands that understand both sides of that equation, that invest in the trust architecture that the fraud environment makes necessary and that treat verified credibility as a competitive asset rather than a compliance obligation, are building positions in a market that will compound their investment as it matures. The brands that do not will find the market progressively less accessible as the retail audience's fraud awareness and verification standards continue to rise.